Background

With the launch of Ethereum’s proof of stake (PoS), liquid staking derivative (LSD) tokens have exploded in popularity for people who want to achieve high ETH staking yields without the complexity of personally operating a staking node. Another key benefit for users is that holding a tokenized representation of their stake is becoming an increasingly useful asset in DeFi.

Until recently, various LSDs on the market have achieved similar beacon chain yields - differences are attributable to slight variances in validator performance. This has led the market to differentiate these tokens mostly upon other metrics like liquidity, market discounts, and perceived decentralization.

frxETH’s Innovative approach

The launch of frxETH marked the arrival of a new LSD which has been able to attract competitive liquidity, and much higher yield. Changing the competitive landscape. An innovative AMO design - a key component in understanding the system - allows it to achieve meaningful yield via a mechanism completely unrelated to beacon chain revenue.

While this approach is great for optimizing yield, it is also important for users to note that it alters the makeup of the system from traditional LSDs which are purely staking services, sending 100% of backing ETH to the beacon chain. In this article we will get into exactly what those differences are, where the yield comes from, and any new risks that users should be aware of.

The FrxETH AMO: A Liquidity Flywheel

The frxETH AMO’s purpose is to:

- Generate overall ETH/frxETH liquidity

- Grow protocol owned liquidity (PoL) + farming revenue

- Capture arbitrage profits

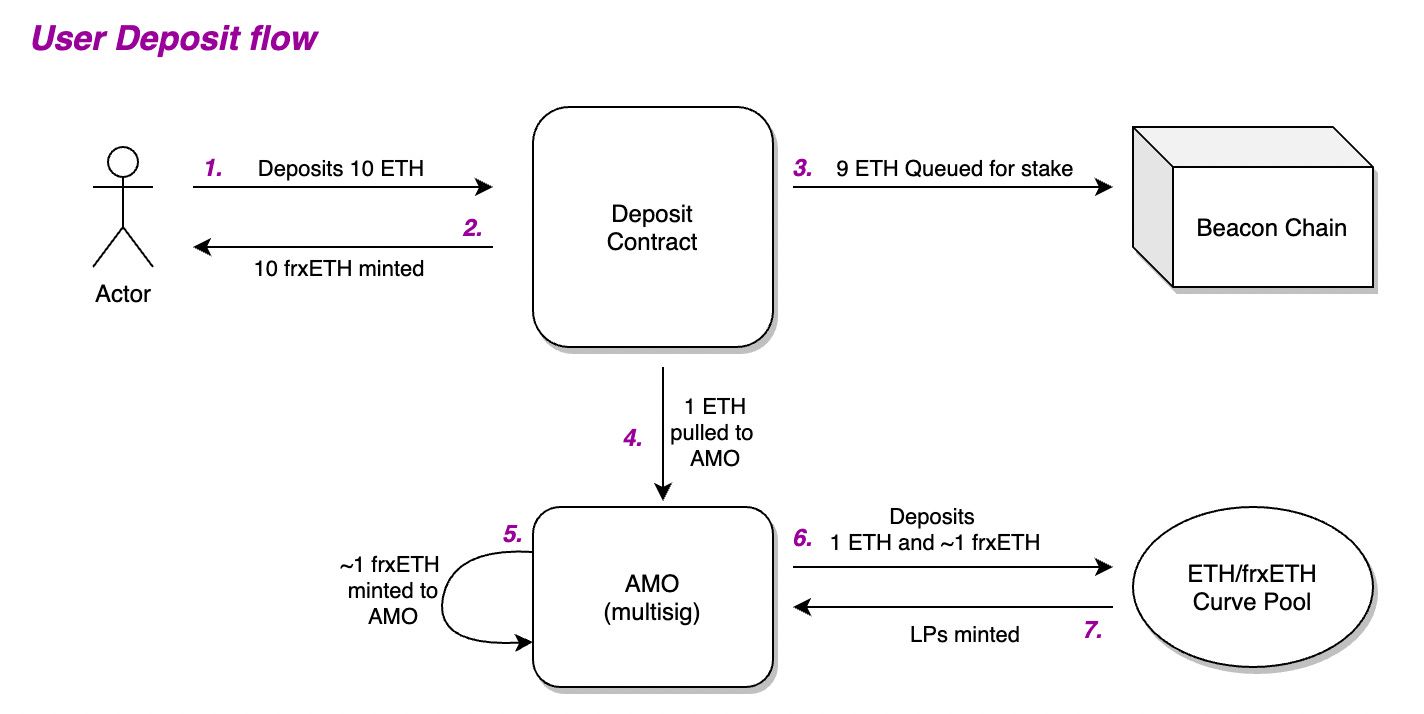

Liquidity for an LSD pair is important for allowing people to enter/exit via the market at low cost while bypassing validator queuing periods. This is why part of the frxETH design is to send 10% of all user deposited ETH to the AMO to be added to the ETH/frxETH curve pool. This amount of ETH is referred to as “Withheld ETH”.

Next, because the AMO has unlimited minting power, it mints an additional frxETH 1:1 for each ETH that has been withheld and then provides both as liquidity into the Curve pool.

Scaling Up the AMO

If we work through this flow for an example user who deposits 10 ETH, we can now expect the following to be true:

- For ever 10 ETH deposited by a user, 11 frxETH are minted (10 to user, 1 to AMO)

- 9 ETH is sent to the beacon chain, with staking yield to be distributed to sfrxETH users

- The AMO provides 1 ETH + 1 frxETH in liquidity to the ETH/frxETH Curve pool

You can imagine that as more users enter frxETH the AMO can grow a very sizeable LP position and therefore is capable of generating significant farming rewards. One of the AMO’s policies is to recycle all earned rewards back into gauge voting bribes, which in turn grows the CRV emissions of the pool. Increased emissions attracts more LPs, and here’s the amazing thing about it:

- When more people exit sfrxETH to provide frxETH liquidity, that means remaining sfrxETH users get higher yield

- When more people provide ETH as liquidity, that means the AMO can mint more frxETH to the LP to balance the pool and generate more farming income

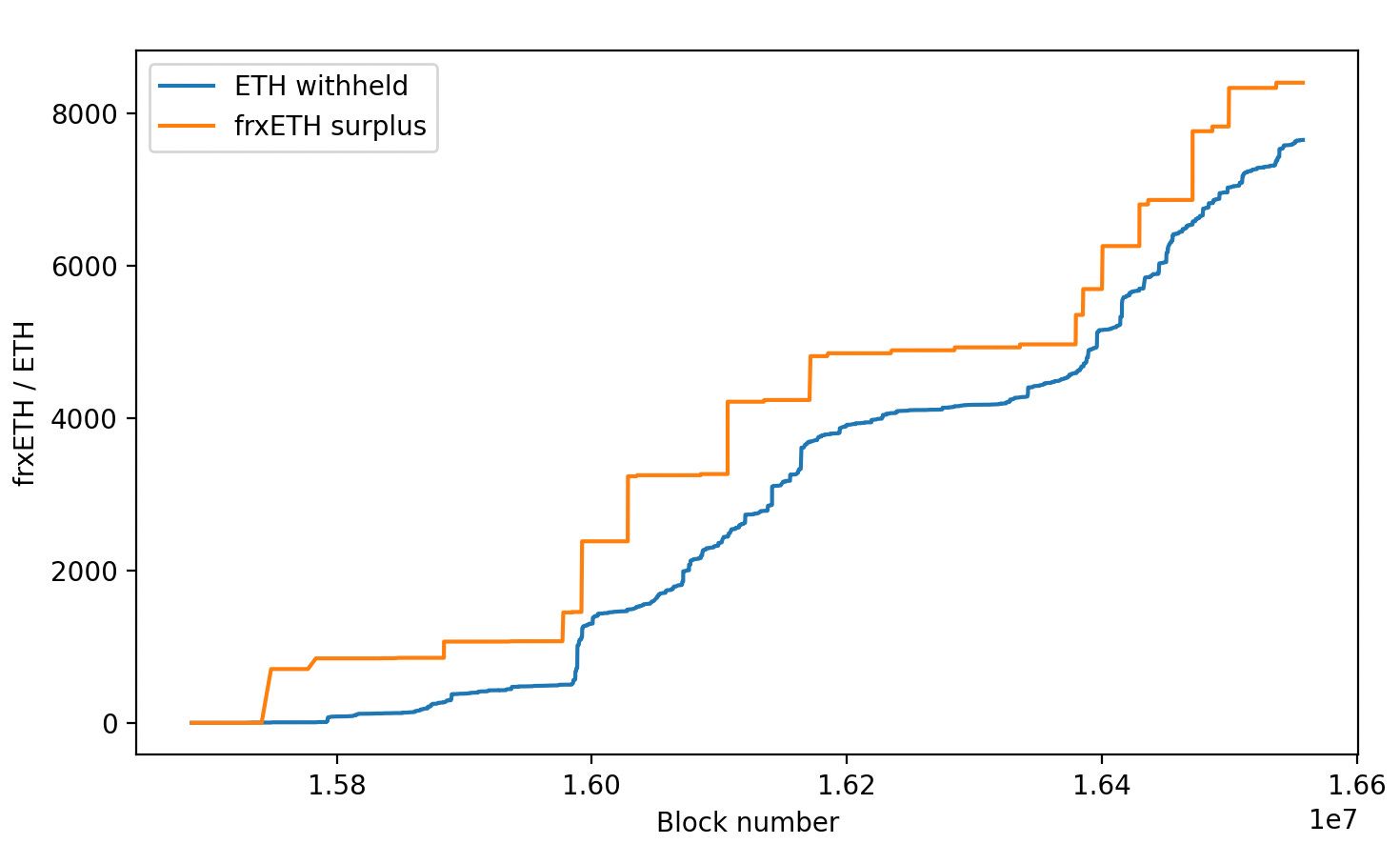

(in the image above you can see actual amount of mints has surpassed the amount of withheld ETH)

Scaling down the AMO

It is important to note that there is a flip side to this activity, which is that as users eventually decide to exit their ETH from system for any reason, the AMO must respond by scaling down using the inverse approach. That is, an outsized amount of frxETH will need to be removed from the pool and burned for every 1 ETH that a user requests to unstake.

In summary , this liquidity provision comes at the cost of reduced overall staked ETH and therefore staking yield for sfrxETH users. But soon we will see why this 10% reduction in yield earning power can be made up for.

Is each frxETH backed 1:1?

Technically, during the course of normal operations, the total supply of frxETH in the system will exceed the amount of ETH in the system (withheld ETH + beacon chain ETH). However, this does not mean that the system is insolvent, or has bad debt. Rather, because the surplus is owned by the AMO’s LP position, it can be removed from the pool at any time to burn the debt and recover the ETH required to match user’s redemption. In fact, if the pool becomes overweight with frxETH, this will allow the AMO to withdraw it and burn this debt at a discount.

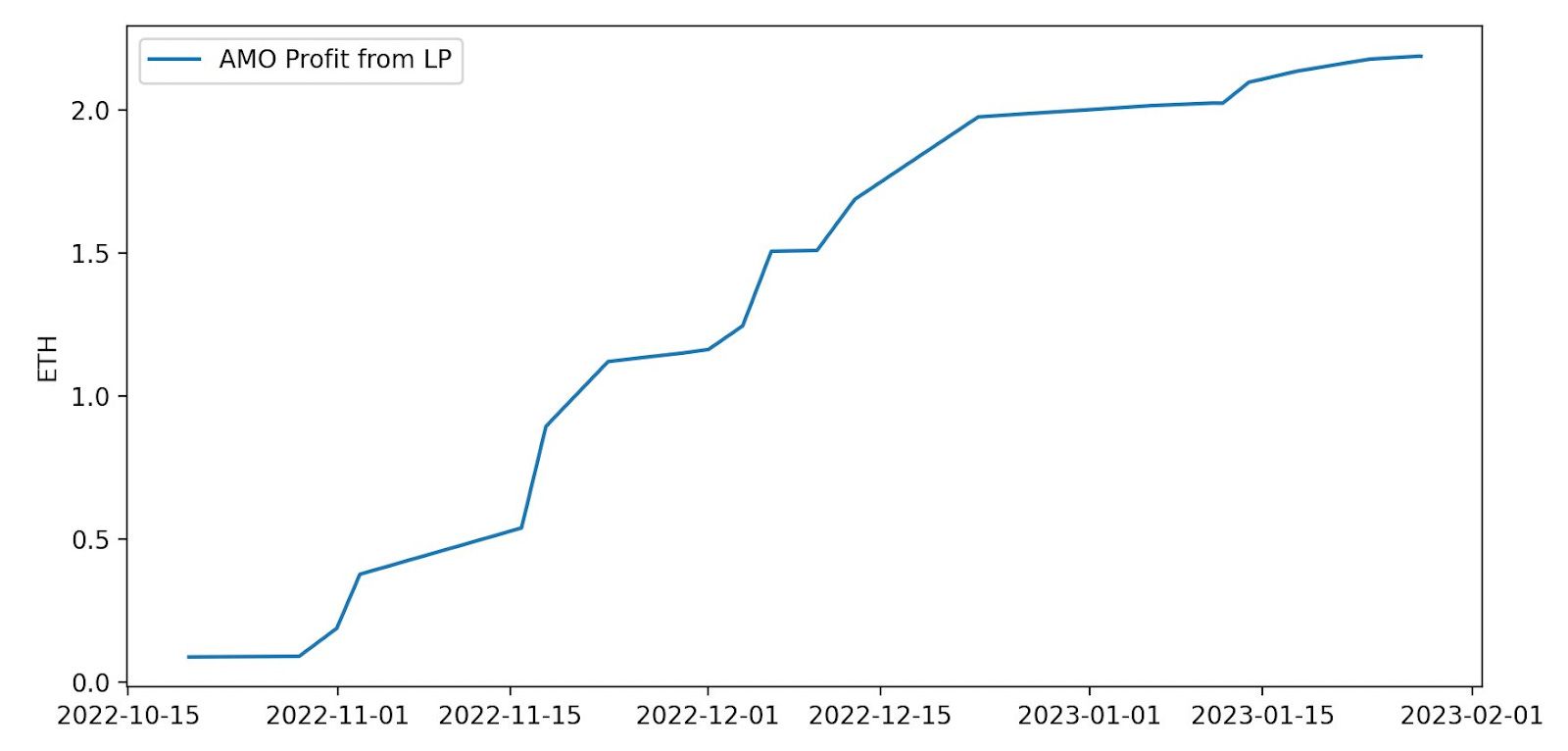

The image below shows the lifetime arbitrage profitability of frxETH AMO’s deposits into the Curve pool. Notice that it has realized zero losses and that it has only generated profits thus far. This means that it has acted in a way which always puts the pool into balance, never out of balance. To date, the AMO has been performing exceptionally well and the system remains fully solvent.

What risks should users look out for?

At the end of the day, the AMO is a simple multisig. The system relies on the good faith of the multisig and its actions. There are currently no smart contracts in place to restrict the behavior of the multisig (e.g. unlimited mint prevention, transfer restrictions, or enforced LP ranges). While the multisig has a great track record thus far, it can do a lot to reduce the amount of trust that users must necessarily place in it.

LPs in the system also bear some risk. If an LP intends to get ETH back out at a good price, it must, to some degree, rely on the AMO (multisig) to act against its own interest to withdraw some of its position from the pool and balance it. The AMO inherently wants to keep a strong position in the pool to maximize farming rewards. The more imbalanced it becomes, the more it stands to profit. So far, the Frax Core team has proven to be good-faith actors when managing the AMO.

Conclusion

So how is frxETH doing in the market today? The yield-optimizing design has proven to be a resounding success, with frxETH growing faster than any other LSD. Today, frxETH market cap is over $150 million and validator count is nearing 2,500 which is significant for a token which was deployed only 4 months ago. With the Shanghai hardfork nearing, beacon chain withdrawals will be enabled and we may see a large reallocation of staked ETH across providers. It will be exciting to monitor how this affects frxETH’s position in the market.

** This article is based on a personal analysis of the frxETH system and should in no way be considered as financial advice