Stablecoins had their moment at ETHDenver, with a packed crowd surrounding the DeFi stage to hear Sam Kazemian’s presentation “Why It's Stablecoins All The Way Down.” The talk comes after critical policy changes for the Frax protocol such as voting to increase its dollar stablecoin collateral ratio to 100%. Additionally, Frax’s ETH-pegged stablecoin frxETH found massive product fit as the fastest growing liquid staking derivative, amassing more than 110,000 ETH staked and claiming the 4th largest position by supply. At a glance, these developments might seem unrelated to each other, but as Kazemian explained, everything in DeFi, whether they know it or not, will become a stablecoin or will become stablecoin-like in structure.

Stablecoin Maximalism Has Entered The Chat

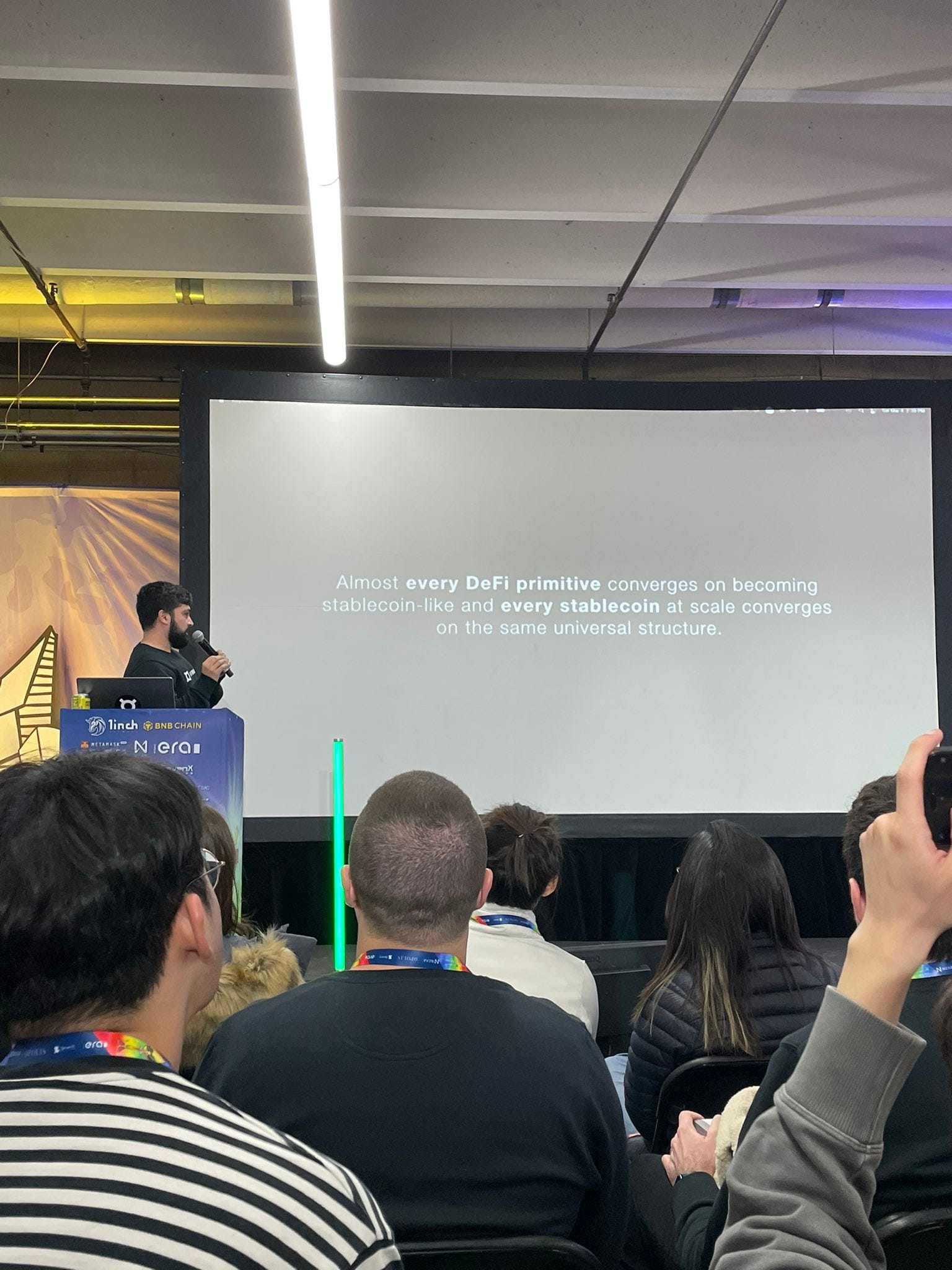

Stablecoin maximalism is the fundamental worldview held by the Frax core team and is the idea that most crypto protocols will converge to become stablecoin issuers in the long-term (or stablecoins become of central importance to their existence). Stablecoin maximalism memetically evolves the concept of The DeFi Trinity that was originally introduced by Frax in early 2022. Instead of a trinity of primitives consisting of a stablecoin, a lending market, and an exchange, stablecoin maximalism abstracts the idea to include ALL of DeFi. Whether a protocol calls itself a bridge, derivatives market, or something else entirely; if its DeFi, then a stablecoin will become foundational to its existence.

The success of a stablecoin can be measured by its monetary premium which is the demand for an issuer’s stablecoin to be held purely for its usefulness without expectation of any interest rate, payment of incentives, or other utility from the issuer. At scale, all stablecoins converge to have the same structure, but what does this structure look like?

Every stablecoin consists of a two part mechanism; the “risk-free yield” and swap facility. The risk-free yield (RFY) is the revenue generated by the assets backing the stablecoin in the lowest risk venue within the system based on its reference peg. The swap facility is where a stablecoin can be redeemed for its reference peg. Both of these parts are essential to maintaining the social contract that exists between stablecoin issuers and stablecoin holders and remains intact as long as the stablecoin can be redeemed for its reference peg in the swap facility.

Stablecoins All The Way Down

Kazemian gave several examples of stablecoins that have this dual structure including USDC, stETH, frxETH, bridged DAI, and FRAX.

Circle’s USDC is a payment stablecoin where the RFY are treasury bills and the swap facility is cash. T-bills are the safest investable collateral asset, since it is guaranteed by the US government. Fiat dollars on their balance sheet provide unparalleled liquidity for the swap facility.

Lido’s stETH is the most popular Ethereum based staking asset at the moment. Its RFY comes from POS validators and the swap facility is the stETH-ETH Curve Pool via $LDO incentives. In the world on-chain, Ethereum’s proof of stake takes the crown as the safest source of yield. Lido currently pays a large amount in subsidies to support liquidity for its Curve pool, which has played a massive role in stETH’s success as the the leading LSD with over 75% market share and millions of ETH staked.

Frax’s frxETH is one of the fastest growing LSD’s on the market right now. Like stETH, the RFY for frxETH are POS validators but the swap facility is the frxETH-ETH Curve Pool via its automated market operator (AMO). For those unfamiliar, AMO are predetermined actions taken by a smart contract to keep a stablecoin at a peg. Frax pioneered AMOs in early 2021 and its Curve AMO has grown to hundreds of millions of dollars and is primary swap facility for the FRAX stablecoin. Frax is now using this proven strategy with frxETH, allowing it to be redeemed for 1 ETH at scale, documented in Flywheel’s most recent Frax Check (and continually so on a weekly basis.)

What makes the frxETH system unique is that it consists of a two-token system that allows it to grow its monetary premium. FrxETH is an ETH-pegged stablecoin while sfrxETH earns native staking yields. Almost 9.5% of all FrxETH in circulation eschews these two high yielding venues and instead is used in various other protocols and networks. For those curious to learn more about how frxETH works, Yearn dev Wavey0x broke down the smart contracts, explaining how the AMO operates.

Kazemian makes an important point that all bridges are stablecoin issuers, using Bridged WrappedDAI as an example. The RFY is the DAI Savings Rate and the swap facility is DAI itself. If there is a sustained monetary premium for Bridged WrappedDAI for its utility on non-Ethereum based networks, then the bridge operator will naturally seek to deposit the underlying asset of DAI in the DAI Savings Rate module.

According to DeFiLlama, the largest bridge is WBTC, a BTC-backed stablecoin that is issued by Bitgo on Ethereum. This categorization of WBTC as a bridged asset is an interesting caveat since Kazemian makes the case that whatever will become the largest bridge will be the one that accrues the most monetary premium. WBTC currently tops the spot with it being used widely throughout DeFi without the use of any incentives from the issuer.

Kazemian shared with the audience that in the future, FRAX will naturally converge on the same universal structure that all fiat-based stablecoins like USDC and USDT have. For FRAX, the RFY will come from T-Bills, FMA/RRPs (frxUSD) and its redeemability will be facilitated in FRAXBP Curve Pool AMOs. In previous interviews, Sam made clear that the only real world asset that Frax aspires to have on its balance sheet are dollars held in a Federal Reserve Master Account. In addition, amid regulatory uncertainty, he clarified that Frax’s recent move to 100% CR backing was because the Frax team believed that the stablecoin maximalist two part mechanism is the superior structure. It's his view that all assets attain fractional reserve backing given sufficient time but only in the manner where the RFY is placed in the lowest risk venue possible.

So what happens to stablecoins that do not converge on this two-prong structure? Kazemian contends that those stablecoins will be unable to scale into the trillions. So far, there is no evidence of alternatives that can prove otherwise and over a long enough time period, those who fail to adopt this structure will lose market share to those who do embrace it.

Monetary Premium Measures Network Effect

The strongest tangible measurement of a stablecoin’s network effect and value accrual is its monetary premium which surpasses brand name, reputation, and other traditional business metrics. The ability to issue currency with value in it of itself is an unforkable concept that is only achieved from years of building utility and trust. It is the reason why Tether is the de facto stablecoin for centralized exchanges, USDC is the most widely used stable in DeFi, and that FRAX and DAI have achieved billions in circulating supply.

While stablecoins will evolve to have different pegs, their underlying structure will remain the same. The first era of stablecoins consisted of commonly accepted dollar-pegged ones such as Tether, USDC, FRAX, and DAI. The second era of stablecoins consisted of established DeFi primitives such as AMMs, lending markets, and veWrappers. The third era that we are currently in consists of liquid staking derivatives, bridges, and other protocol derived assets like GMX’s potential future stablecoin.

Frax Finance, The ‘Stablecoin Maximalist’ Protocol

One statement that Sam repeated throughout the speech is that Frax is extremely consistent on its stablecoin maximalist worldview. At the end of the day, Frax Finance is a stablecoin protocol that issues innovative decentralized stablecoins and builds the subprotocols to support them. Presently, this three stablecoins FRAX, FPI, and frxETH, supported by integrations in Fraxlend, Fraxswap, and Fraxferry.

Stablecoins are one of the most important infrastructure pieces in all of crypto and everything Frax builds and ships is with the intention of achieving the highest monetary premium in the safest manner at scale. Through the protocol’s underlying philosophy of stablecoin maximalism, within 5-10 years, the Frax family of stablecoins aims to achieve hundreds of billions if not trillions of dollars in TVL.

Whether you know it or not anon, at the end of the day, it’s all stablecoins.